Why the Fundus Camera Market Is Becoming Essential to the Future of Eye Care

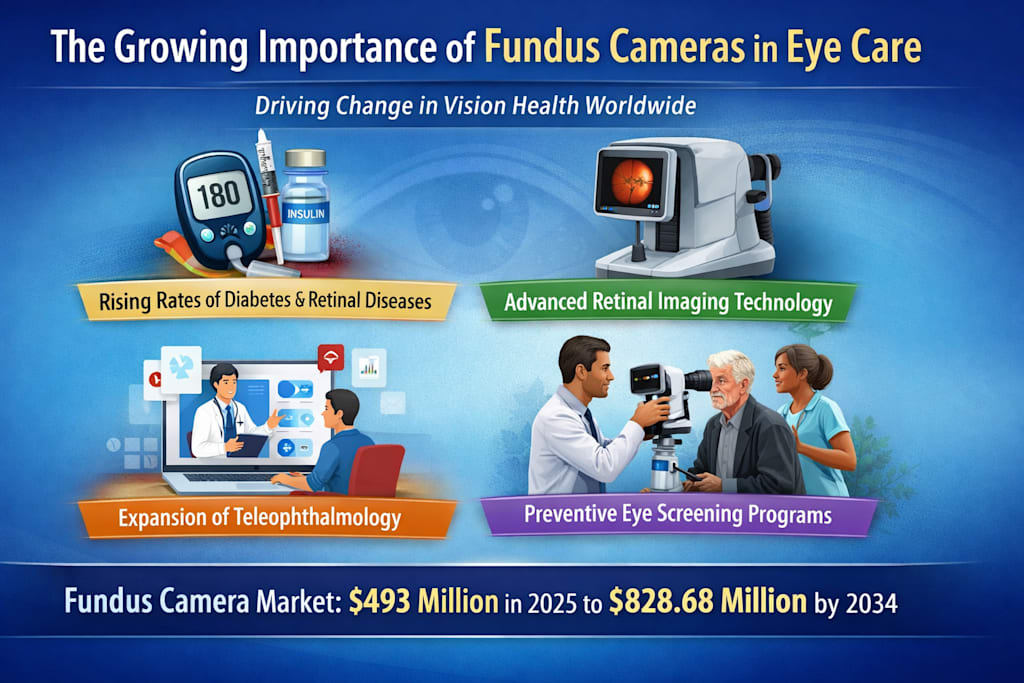

As diabetes, retinal disease, and preventive screening programs rise worldwide, fundus cameras are moving from specialist tools to frontline healthcare essentials.

The Silent Eye Health Crisis Driving a New Wave of Medical Innovation

Most people do not think about retinal imaging until a doctor tells them something is wrong.

That is exactly why the global fundus camera market is gaining attention. These devices, once used mainly inside specialist ophthalmology clinics, are now becoming critical across hospitals, outpatient centers, telemedicine programs, and even community-based screening networks. Their growing importance reflects a broader healthcare shift: moving from late-stage treatment to early detection.

According to Renub Research, the Fundus Camera Market is expected to rise from US$ 493 Million in 2025 to US$ 828.68 Million by 2034, expanding at a CAGR of 5.94% from 2026 to 2034. That trajectory is not just about technology upgrades. It points to a global increase in retinal disorders, diabetes-related eye complications, ageing populations, and the urgent need for accessible vision screening

In many ways, fundus cameras are becoming one of the most practical and powerful tools in modern preventive eye care.

What a Fundus Camera Actually Does — and Why It Matters

A fundus camera is designed to capture high-quality images of the inside surface of the eye, known as the fundus. This includes the retina, optic disc, macula, and blood vessels. These images help doctors detect and monitor conditions such as diabetic retinopathy, glaucoma, age-related macular degeneration, retinal vein occlusion, and hypertensive retinopathy

That may sound technical, but the value is simple: these cameras help doctors see problems before patients feel them.

In many eye diseases, damage begins quietly. A patient may still have “normal” vision while underlying retinal changes are already progressing. Fundus cameras make those invisible warning signs visible. This allows physicians to intervene earlier, often before permanent vision loss occurs.

That early-detection capability is becoming more important every year.

A World with More Diabetes Means a World with More Retinal Risk

One of the strongest growth drivers in this market is the increasing burden of chronic disease, especially diabetes and hypertension.

As diabetes rates continue to climb globally, the number of people at risk for diabetic retinopathy also rises. This condition can damage the retina over time and, if left untreated, may lead to irreversible blindness. The challenge is that many patients do not notice symptoms in the early stages. By the time vision changes occur, the disease may already be advanced.

That is where fundus cameras play a major role.

Instead of relying only on symptom-based care, healthcare providers can use retinal imaging as part of routine screening. This makes it easier to catch damage early and start treatment sooner. It also lowers the long-term cost burden on healthcare systems by reducing preventable complications.

The broader scale of the issue is significant. The material you provided notes that global vision impairment remains widespread, with major causes including cataracts, refractive errors, age-related macular degeneration, glaucoma, and diabetic retinopathy

The implication is clear: eye care is no longer a niche specialty issue. It is becoming a mainstream public health priority.

Technology Is Making Retinal Imaging Faster, Smarter, and More Accessible

Another major reason the fundus camera market is expanding is the speed of technological progress.

Older retinal imaging systems often required dilation, more clinical time, and specialist workflows. Today’s newer devices are increasingly digital, portable, non-mydriatic, AI-enabled, and telehealth-compatible. That changes everything.

Non-mydriatic fundus cameras

These devices can often capture retinal images without dilating the pupil, which makes the process quicker and more comfortable for patients. In busy clinics or screening camps, that matters a lot.

Portable and handheld systems

Handheld fundus cameras are especially valuable in rural outreach, primary care, home visits, and mobile health programs. They help expand eye screening beyond large urban hospitals.

AI-assisted imaging

Artificial intelligence is also entering the space. AI-enabled systems can help flag retinal abnormalities, improve screening efficiency, and support clinicians in identifying patients who need urgent follow-up.

Cloud and digital integration

Modern systems can connect with electronic health records, teleophthalmology platforms, and remote consultation workflows. That means an image captured in a village clinic can be reviewed by a specialist in a major city.

This is not just a device upgrade story. It is a care delivery transformation.

Why Preventive Eye Screening Is Becoming a Bigger Priority

Healthcare systems worldwide are increasingly shifting toward prevention, and retinal imaging fits perfectly into that strategy.

Governments, NGOs, hospitals, and community health programs are placing more emphasis on routine eye screening, especially for high-risk populations such as older adults and people living with diabetes. Fundus cameras make these programs scalable because they offer standardized, recordable, and reviewable eye images.

This is especially useful in teleophthalmology, where images captured locally are interpreted remotely by specialists.

That model has become more relevant in underserved areas, where access to ophthalmologists may be limited. Instead of requiring every patient to travel long distances for specialist care, providers can bring screening closer to the patient.

This is a powerful shift because it improves access without compromising diagnostic quality.

In practical terms, fundus cameras are helping healthcare systems answer a difficult question:

How do you screen more people for eye disease without overwhelming specialists?

Increasingly, this technology is part of the answer.

The Market Still Faces Real Barriers

Even with strong growth potential, the fundus camera market is not without challenges.

High equipment cost

Advanced imaging systems — especially wide-field and high-resolution digital units — can be expensive. Beyond the purchase price, providers must also consider software updates, maintenance, staff training, and integration costs. This creates a barrier for smaller clinics and resource-constrained healthcare systems

Need for trained personnel

Capturing a high-quality retinal image is not always as simple as pressing a button. Image quality, patient positioning, and workflow efficiency still depend on training. In many emerging markets, there is a shortage of skilled operators and specialists.

Workflow integration

Some facilities also struggle with integrating imaging tools into existing clinical systems. If the technology adds friction instead of reducing it, adoption can slow down.

So while the opportunity is strong, success in this market will depend not only on innovation but also on affordability, usability, and implementation support.

Which Types of Fundus Cameras Are Seeing Demand?

The market is not built around one single device category. Different healthcare settings need different imaging solutions.

Mydriatic fundus cameras

These are typically used when providers need maximum image clarity and detailed retinal visualization. They are common in hospitals and specialist eye centers, especially for more complex retinal conditions

Non-mydriatic fundus cameras

These are becoming increasingly popular because they are faster, more patient-friendly, and easier to deploy in high-volume settings.

Hybrid fundus cameras

These systems offer flexibility and can help facilities manage a wider range of patient needs.

ROP fundus cameras

A particularly important segment is ROP (Retinopathy of Prematurity) fundus cameras, which are used for screening premature and low-birth-weight infants. This is a highly specialized but growing area, especially as neonatal screening programs expand

Each segment serves a different clinical need, which means manufacturers that can tailor solutions to real-world care environments are likely to remain competitive.

Where Is Demand Coming From? Clinics, Hospitals, and Beyond

Two major end-user groups are driving adoption: ophthalmology clinics and hospitals.

Ophthalmology clinics

These remain one of the most active use cases because retinal imaging is now central to routine examinations, disease monitoring, and treatment planning. Clinics especially value compact and efficient systems that support faster patient flow.

Hospitals

Hospitals use fundus cameras not only in eye departments but also in emergency medicine, internal medicine, and neurology, where retinal changes can reveal systemic disease. Hospitals typically prefer robust systems with strong imaging performance and digital integration.

A growing third layer: decentralized care

What is changing fastest, however, is the expansion of retinal imaging into community care, outreach programs, primary care settings, and telemedicine networks.

That is where the next wave of growth may become especially visible.

Regional Momentum: Why the U.S., Germany, India, and Saudi Arabia Matter

Different countries are shaping the market in different ways.

United States

The U.S. remains one of the most significant markets because of its large diabetic population, preventive care focus, strong medical technology ecosystem, and high adoption of AI-enabled and wide-field imaging systems

Germany

Germany’s market is driven by diagnostic quality, clinical evidence, and structured healthcare delivery. Adoption is shaped by regulation, but the market remains strong for high-quality ophthalmic imaging.

India

India stands out as one of the most important long-term growth markets. The country faces a high burden of diabetes, preventable vision loss, and unequal access to specialist care. This makes portable, affordable, and teleophthalmology-compatible fundus cameras particularly relevant. Government programs, nonprofit outreach, and public-private partnerships are all helping push adoption forward

Saudi Arabia

Saudi Arabia is also emerging as an important market due to rising diabetes prevalence, healthcare investment, and national interest in preventive care.

These country-level dynamics show that the market is not being driven by one trend alone. Instead, it is being shaped by a combination of disease burden, healthcare infrastructure, digital readiness, and screening policy.

What This Market Really Signals About the Future of Healthcare

The growth of the fundus camera market is about more than one device category. It reflects a broader transformation in healthcare delivery.

It shows that:

Diagnosis is moving earlier

Imaging is becoming more decentralized

AI is entering routine care

Screening is becoming more scalable

Telemedicine is becoming more practical

In short, healthcare is moving closer to patients — and fundus cameras fit that future extremely well.

As eye disease continues to rise globally, the systems that succeed will be the ones that can combine accuracy, affordability, speed, and accessibility. Fundus cameras are increasingly positioned at that intersection.

That is why this market deserves more attention than it gets.

Because in the years ahead, protecting vision will depend less on waiting for symptoms and more on seeing risk early — clearly, quickly, and at scale.

Final Thoughts

The Fundus Camera Market is not just growing because healthcare providers want better equipment. It is growing because the world needs better, earlier, and more inclusive eye care.

With Renub Research projecting the market to reach US$ 828.68 Million by 2034, this segment is becoming one of the more meaningful examples of how medical imaging, digital health, and preventive care are converging

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Why the All-Terrain Vehicle Market Is Gaining Ground Across Recreation, Farming, and Defense

There was a time when all-terrain vehicles (ATVs) were seen mostly as machines for thrill-seekers — the kind of vehicle you’d expect to find tearing through muddy trails, sandy dunes, or forest tracks on a weekend getaway. But that image is changing rapidly.

By shibansh kumarabout 12 hours ago in Trader

Fannie Mae Stock Insights What UK Investors Should Know in 2026

Fannie Mae stock has become an important focus for UK investors who follow global markets. Its connection to the US housing market and government policies makes it both interesting and unpredictable. Understanding Fannie Mae stock helps investors make informed decisions and avoid unnecessary risks.

By John.doe798a day ago in Trader

Mexico Autonomous Trucks Market Size to Hit USD 1,551.84 Million by 2034

Mexico Autonomous Trucks Market Size, Growth, and Forecast (2026–2034) The Mexico autonomous trucks market is gaining strong momentum as the logistics and transportation sector undergoes rapid technological transformation. In 2026, the market reflects increasing adoption of automation to address efficiency challenges and rising freight demand.

By Jackson Watson4 days ago in Trader

Bibbidi-Bobbidi-Booyah!

Dear Professor Donkeldong, I would like to formally apologize. Last night I snuck into your office. I sat in your chair and poured myself three fingers of Scotch from the bottle you’ve got stashed in the top desk drawer. Then I helped myself to your private library.

By Leslie Writes7 days ago in Humor

Comments

There are no comments for this story

Be the first to respond and start the conversation.