Europe Next Generation Sequencing Market Set for Transformative Growth Through 2034

Precision medicine, oncology breakthroughs, and genomic innovation are accelerating Europe’s next wave of healthcare transformation

Europe’s healthcare and life sciences ecosystem is entering a defining era, and at the center of this shift is Next Generation Sequencing (NGS). Once viewed primarily as a specialized research tool, NGS is now becoming an essential pillar of modern medicine, powering everything from cancer diagnostics and rare disease detection to drug discovery and personalized treatment planning.

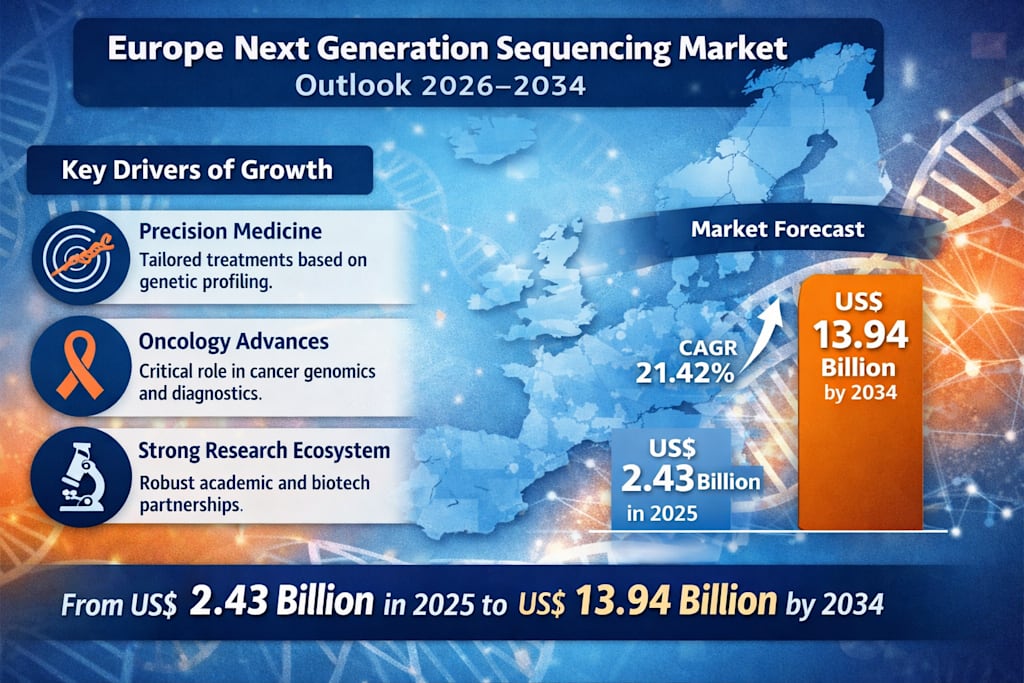

According to Renub Research, the Europe Next Generation Sequencing Market is projected to rise from US$ 2.43 billion in 2025 to US$ 13.94 billion by 2034, expanding at a remarkable CAGR of 21.42% during 2026–2034. That trajectory reflects far more than a fast-growing technology segment. It signals a broad healthcare transformation driven by better data, earlier diagnosis, and more targeted care.

What makes this market particularly compelling is that Europe is not just adopting NGS—it is building an ecosystem around it. Governments, research institutes, biotech firms, hospitals, and pharmaceutical companies are all helping to expand the role of sequencing in both research and real-world clinical care.

Why NGS is becoming essential in modern healthcare

At its core, Next Generation Sequencing is a powerful technology that enables rapid, high-throughput sequencing of DNA and RNA. Unlike older sequencing methods that processed genetic material in a slower, more limited way, NGS can analyze millions of fragments simultaneously. This allows scientists and clinicians to study entire genomes, exomes, and targeted gene panels with impressive speed and precision.

That capability has changed the rules of genomic science. Instead of focusing on one gene at a time, researchers and clinicians can now gain a broader, more detailed picture of disease biology. This matters enormously in fields such as oncology, inherited disorders, infectious disease surveillance, and pharmacogenomics, where subtle genetic differences can influence diagnosis, treatment, and outcomes.

Europe has become fertile ground for this expansion. The region benefits from a strong scientific base, respected academic institutions, cross-border research collaborations, and increasing policy support for genomic medicine. Countries such as Germany, the United Kingdom, France, and the Netherlands are already showing how NGS can be integrated into both research and healthcare systems.

Precision medicine is pushing demand to a new level

One of the strongest forces behind the Europe NGS market is the rise of precision medicine. Traditional medicine often relies on generalized treatment pathways, but precision medicine seeks to tailor care based on a patient’s unique genetic profile. NGS makes that possible at scale.

In Europe, this shift is becoming especially visible in oncology, rare disease diagnosis, and inherited condition management. Rather than treating all patients with a similar diagnosis the same way, clinicians can increasingly use sequencing data to identify the most effective therapies for specific molecular subtypes. This can improve outcomes, reduce trial-and-error prescribing, and help healthcare systems move toward more efficient care delivery.

Government-backed genomic programs are also reinforcing this trend. Europe has been actively investing in precision medicine initiatives designed to bring genomic data into mainstream care. One example noted in the market material is EP PerMed, the European Partnership for Personalised Medicine, which was formally launched in Valencia in October 2023. With 49 partners, the initiative aims to support innovation, knowledge transfer, and healthcare integration across the region.

That matters because markets grow faster when infrastructure, policy, and clinical use cases evolve together—and that is exactly what is happening here.

Oncology and rare disease testing are major growth engines

If there is one clinical area where NGS is already proving its value at scale, it is cancer. Europe continues to face a substantial cancer burden, and the demand for more accurate, earlier, and more personalized diagnostics is rising accordingly.

NGS allows clinicians and researchers to analyze tumor genetics in much greater detail than many conventional testing methods. It can identify mutations, biomarkers, and molecular signatures that influence both prognosis and treatment selection. That makes it particularly valuable for precision oncology, where the right therapy often depends on understanding the tumor at a genomic level.

The opportunity extends well beyond oncology. Rare diseases, many of which have a genetic basis, are another major driver of NGS adoption. Families often spend years searching for a diagnosis when symptoms are unclear or traditional tests come back inconclusive. NGS can shorten that diagnostic journey by detecting rare or complex variants more efficiently.

As healthcare providers and policymakers increasingly recognize this value, NGS is moving from niche specialty testing toward broader clinical integration across Europe.

Europe’s research ecosystem gives the market a structural advantage

A major reason the European NGS market looks so strong over the long term is that its growth is supported by a deep research and innovation ecosystem. This is not a market being built on hype alone. It is being supported by public funding, institutional expertise, and real-world translational science.

European academic institutions, biotechnology firms, and public research programs are investing heavily in genomics, transcriptomics, metagenomics, and epigenetics. These areas depend heavily on sequencing technologies, and their expansion naturally increases demand for NGS instruments, reagents, software, and services.

The file also highlights how programs such as Genomics England’s Newborn Genome Programme are helping expand the role of sequencing in early detection and preventive care. Meanwhile, the European Health and Digital Executive Agency (HaDEA) has announced new funding opportunities under the 2025 EU4Health Work Programme, further strengthening Europe’s preparedness and long-term health innovation capabilities.

This creates a strong feedback loop: more funding leads to more sequencing activity, which leads to more data, more validation, more clinical trust, and broader adoption.

The market is expanding across instruments, services, diagnostics, and drug discovery

One of the most interesting aspects of the Europe NGS market is that growth is not limited to a single product category. Instead, it is unfolding across multiple parts of the value chain.

Instruments remain foundational

Sequencing instruments continue to be a major market component, particularly as research laboratories, clinical testing centers, and pharmaceutical companies seek faster and more versatile platforms. Europe’s labs increasingly need systems capable of handling oncology testing, infectious disease studies, whole-genome sequencing, and targeted panels. Even though these instruments remain capital-intensive, ongoing funding and adoption are helping drive sales.

Services are becoming increasingly attractive

NGS services are also gaining momentum, especially among institutions that want sequencing capabilities without making large upfront investments in equipment and in-house bioinformatics teams. Outsourcing sequencing, sample preparation, and reporting has become an efficient option for hospitals, biotech firms, and research organizations. As genomic data becomes more complex, service providers offering end-to-end support are becoming even more valuable.

Diagnostics is where commercial potential gets even bigger

NGS-based diagnostics may ultimately become one of the most commercially significant parts of the market. In Europe, sequencing is increasingly being used in cancer diagnostics, prenatal testing, rare disease screening, and infectious disease applications. As awareness grows and reimbursement conditions improve in some countries, diagnostics adoption is likely to deepen further.

Drug discovery is another high-growth lane

The pharmaceutical industry is also helping fuel the NGS boom. Sequencing technologies are now central to identifying drug targets, understanding biomarkers, segmenting patient populations, and supporting companion diagnostics. For drug developers, NGS can help improve R&D productivity while supporting the broader shift toward targeted therapies and precision therapeutics.

Technology platforms are evolving—and that will shape competition

Within the European market, not all sequencing technologies are growing at the same pace. The file notes that Sequencing by Synthesis (SBS) remains the most widely used NGS technology in the region, largely because of its high accuracy and broad applicability across whole-genome, targeted, and RNA sequencing workflows. Its established reliability continues to make it the preferred platform for many labs and institutions.

At the same time, Ion Semiconductor Sequencing is also finding its place, particularly in targeted sequencing and diagnostic workflows where speed and ease of operation are valuable. While it may not yet match SBS in overall dominance, its suitability for medium-scale labs and fast-turnaround applications gives it meaningful market relevance.

As newer methods such as nanopore and single-molecule approaches continue to evolve, competition across technology platforms could intensify, creating even more innovation across the European genomics space.

Hospitals and clinics are becoming more important end users

NGS is no longer confined to specialized research centers. One of the clearest signs of market maturity is the growing adoption of sequencing technologies in hospitals and clinical settings.

Across Europe, hospitals and clinics are increasingly incorporating NGS into oncology workflows, rare disease diagnostics, and broader personalized medicine strategies. This transition is important because it shifts sequencing from an exploratory technology into a practical tool for patient care. When hospitals adopt NGS at scale, it creates recurring demand not just for equipment, but also for consumables, software, interpretation tools, and diagnostic support services.

This also means that future winners in the NGS market may be those companies that make sequencing easier to deploy in real clinical environments—not just those with the fastest machines.

Country-level momentum is adding strength to the regional outlook

Europe’s NGS story is not uniform, but several key markets are providing major momentum.

Germany remains a leader thanks to its strong research institutions, advanced healthcare infrastructure, and active use of NGS in oncology, rare diseases, and pharma research. The file notes that QIAGEN plans to launch three sample preparation instruments during 2025 and 2026, reinforcing Germany’s role in supporting next-generation genomics workflows.

France is also strengthening its position through precision medicine programs and rising diagnostic adoption. The file highlights Devyser’s February 2025 launch of Devyser Thalassemia v2, a platform aimed at simplifying genetic analysis and improving structural variation detection.

The United Kingdom continues to stand out due to its large-scale genome initiatives and NHS-linked adoption. The file points to Almac Diagnostic Services’ August 2023 upgrade of its NGS offering, including installation of the first Illumina NovaSeq X Plus in Northern Ireland and across the island of Ireland.

Even emerging markets such as Russia are gradually expanding their genomics capabilities, suggesting that the broader European opportunity is still developing and not yet fully mature.

The biggest barriers are still real—and they matter

For all its promise, the Europe NGS market is not without challenges.

The first is cost. While sequencing itself has become less expensive over time, the full NGS ecosystem still requires significant investment. Instruments, reagents, consumables, computational infrastructure, storage systems, and skilled bioinformatics personnel all add to the cost burden. For smaller hospitals and laboratories, that can slow adoption.

The second challenge is regulation and privacy. Europe has some of the world’s strongest data protection rules, and genomic data is among the most sensitive categories of personal information. Complying with privacy frameworks such as GDPR can add administrative complexity and operational cost, particularly for companies working across multiple countries. Regulatory approval for clinical applications can also be time-consuming.

These challenges are real, but they are not likely to stop the market. More likely, they will shape which companies are best positioned to scale successfully.

Final Thoughts

The Europe Next Generation Sequencing Market is no longer a future-facing niche. It is rapidly becoming one of the most important pillars of modern healthcare and biomedical innovation.

With Renub Research forecasting growth from US$ 2.43 billion in 2025 to US$ 13.94 billion by 2034, the market is on a trajectory that reflects deep structural change, not just temporary demand. Precision medicine, cancer diagnostics, rare disease testing, genomic research, and drug discovery are all converging to create a powerful long-term opportunity.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Why the United States Medical Ceramics Market Is Quietly Becoming a Major Healthcare Growth Story

These advanced materials are increasingly becoming essential in modern medicine because they offer something every healthcare system wants more of: durability, biocompatibility, precision, and long-term performance. Whether used in hip replacements, dental implants, bone grafts, surgical tools, or reconstructive procedures, medical ceramics are helping improve patient outcomes while supporting the next generation of medical innovation.

By shibansh kumarabout 7 hours ago in Trader

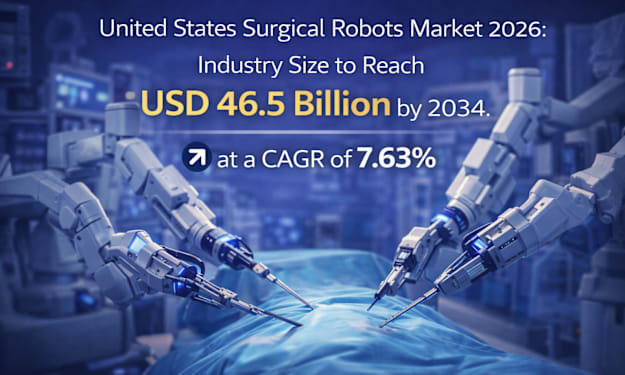

United States Surgical Robots Market Size, Share & Growth Outlook to 2034

United States Surgical Robots Market Size, Growth, and Forecast (2026–2034) The United States surgical robots market is experiencing steady expansion as healthcare systems increasingly adopt advanced technologies to improve patient outcomes. The market reached a value of USD 23.2 Billion in 2025 and is projected to grow significantly, reaching USD 46.5 Billion by 2034, exhibiting a CAGR of 7.63% during 2026–2034.

By Jackson Watsona day ago in Trader

GRANDMA NELSON

Daddy pulled off the interstate, and I saw the all familiar red barn, and I knew we had arrived at Grandma Nelson's farm. I always had mixed feelings about seeing my Grandmother. It seemed she had as many Grandchildren as the old Mother in the shoe nursery rhyme. I saw her as different, but that is not why I hestiated. The truth be known I always got in trouble at her house, and ended up sitting in the car after I had been scolded.

By Susan Payton7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.