Agricultural Biologicals Market Trends: Microbial Solutions & Forecast to 2033

Rising demand for sustainable farming, microbial crop protection, and biofertilizers is accelerating innovation and investment in the global agricultural biologicals market.

Growing concerns over chemical residues in food, mounting regulatory pressure on synthetic pesticides, and a sharp rise in consumer demand for organic and residue-free produce are collectively pushing agricultural biologicals into the mainstream. Once considered a niche or complementary input, biopesticides, biofertilizers, and biostimulants are now central to how forward-thinking farmers manage crops — from large-scale row-crop operations in North America to smallholder fruit and vegetable farms across Asia Pacific.

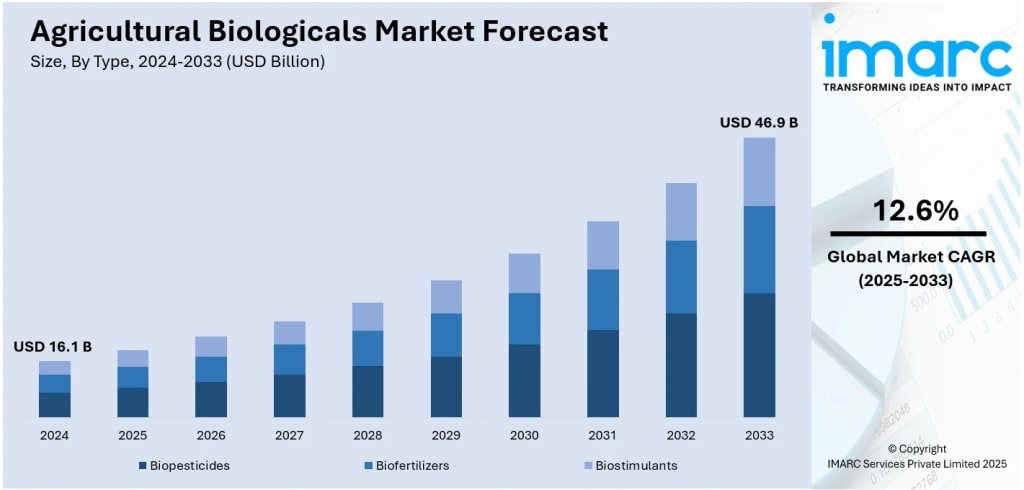

According to IMARC Group’s latest research, the global agricultural biologicals market was valued at USD 16.1 Billion in 2024 and is projected to reach USD 46.9 Billion by 2033, at a CAGR of 12.6% during 2025–2033. North America currently leads with a 32.1% market share, driven by strong government support, a mature organic farming sector, and robust R&D infrastructure. As sustainability becomes a non-negotiable pillar of global agriculture, the adoption of biological inputs is accelerating across every major region.

Agricultural Biologicals Market — Key Statistics at a Glance

The agricultural biologicals market has been expanding rapidly as farmers shift toward sustainable and eco-friendly crop protection methods. Industry data suggests that the market was valued at USD 16.1 billion in 2024 and is expected to grow significantly, reaching around USD 46.9 billion by 2033. This growth reflects a strong compound annual growth rate (CAGR) of about 12.6% between 2025 and 2033, highlighting the increasing adoption of biological farming inputs across global agriculture.

Regionally, North America currently leads the market, accounting for around 32.1% of the total share in 2024. This leadership position is largely supported by strong government initiatives, advanced agricultural technologies, and a well-established organic farming industry.

From a product perspective, biopesticides represent the largest segment, as farmers increasingly prefer natural pest control solutions that reduce chemical residues in crops. When looking at the source of these biological products, microbial-based solutions dominate, representing about 51.8% of the market, due to their effectiveness in improving soil health and crop protection.

In terms of application methods, foliar spray remains the most widely used technique, accounting for approximately 58.5% of applications globally. This method allows farmers to deliver biological inputs directly to plant surfaces, improving efficiency and crop response.

Crop-wise, the fruits and vegetables segment holds the largest share at roughly 48.7%, since these crops often require stricter residue standards and higher-quality produce for both domestic consumption and export markets.

Request a Business Sample Report for Procurement & Investment Evaluation

Agricultural Biologicals Market Growth Drivers

Surging Demand for Sustainable and Organic Farming Practices

Organic farming is no longer a fringe movement — it’s a rapidly growing segment of mainstream agriculture. U.S. sales of certified organic products came close to USD 70 Billion in 2023, according to the Organic Trade Association, and domestic organic farmland grew 15% in the same year per USDA data. In Europe, the organic food market reached USD 57.5 Billion. This shift means farmers are increasingly turning to biopesticides and biofertilizers to meet residue-free standards, satisfy retailer requirements, and tap into premium pricing. Governments are backing this transition: the EU’s Farm to Fork Strategy targets a 50% reduction in chemical pesticide use by 2030, while programs like the USDA’s Organic Transition Initiative offer direct financial support to producers seeking certification.

Regulatory Crackdown on Synthetic Chemicals and Pesticide Resistance

Regulatory headwinds against conventional agrochemicals are intensifying, opening doors for biological alternatives. The EPA has been actively streamlining biostimulant registration pathways to reduce time-to-market for new biological products. Meanwhile, in May 2024 alone, the EPA approved 12 new biological registrations in a single month — the highest on record. Pesticide resistance is adding further urgency: over 600 arthropod species now show resistance to at least one pesticide class, and yield losses tied to resistance exceeded USD 1.8 Billion in 2024. With resistance to neonicotinoids and organophosphates rising in key pests like corn rootworm and soybean aphid, integrated pest management programs are increasingly recommending biologicals as essential rotation partners.

Government Schemes and Public Investment in Biological Agriculture

Supportive policy is proving to be a powerful market accelerant. In India, the September 2024 approval of the Bio-RIDE scheme by the Union Cabinet — aimed at boosting biotechnology R&D and biomanufacturing — directly targets agricultural biologicals, including bio-agri inputs and climate-resilient crop solutions. In October 2024, India also launched its first Biomanufacturing Institute for Agri-Food Innovation (BRIC-NABI) to fast-track biopesticide and biofertilizer commercialization. The European Commission allocated €1.5 Billion for sustainable agriculture research in 2024, while China unveiled new biotechnology cultivation guidelines in early 2025 focused on advanced bio-inputs for wheat, corn, soybean, and rapeseed. These government-backed frameworks are giving industry players the confidence to invest at scale.

Agricultural Biologicals Market Trends

Biopesticides Lead, Biostimulants Pick Up Speed

Biopesticides remain the dominant product category, accounting for over 50% of market share in 2024, driven by their effectiveness in managing pests without leaving toxic residues. But it’s the biostimulants segment that’s generating the most excitement right now. Demand for biostimulants in Europe alone grew by over 12% in 2024, according to the European Biostimulants Industry Council (EBIC), led by the cereal and vegetable segments. The appeal is clear: biostimulants help crops tolerate drought, salinity, and temperature extremes — challenges that are only getting more acute with climate change. In February 2025, UPL launched “Zeba Bioboost,” a biopolymer-based biostimulant for arid regions that showed up to 18% yield improvement in pilot programs across India and Latin America for drought-prone crops like maize and soybean.

Strategic M&A and Partnerships Reshaping the Competitive Landscape

The agricultural biologicals space is in the middle of a deal-making boom. Major agrochemical companies are actively acquiring and partnering to build out their biological portfolios rather than develop everything in-house. In October 2024, Corteva completed the Symborg acquisition, adding nitrogen-fixing microbes to its seed-treatment lineup. In July 2025, UPL launched Nuvita in Brazil under its Natural Plant Protection platform, while Bayer signed an exclusive distribution agreement with France-based M2i Group to commercialize pheromone gels across Asia-Pacific, Latin America, and the U.S. Close to 45% of biological industry deals are inked by European players, according to sector analysts, with more than 1,300 patents related to agricultural biologicals filed since 2019 — approximately 75% of them focused on developing novel biologic crop solutions.

Precision Agriculture and Digital Tools Accelerating Biological Adoption

Getting the most out of agricultural biologicals requires precise timing and application — and that’s where digital agriculture is playing a critical role. Variable-rate sprayers now cover roughly 23% of row-crop acres in North America, enabling targeted microbial delivery that can lift field-level returns. IoT-linked storage systems help farmers maintain product viability by monitoring temperature in real time, preventing the performance losses that have historically dampened confidence in biologicals. Early adopters are reporting input cost reductions of around 15% without sacrificing yields. The integration of AI-driven pest models and weather data platforms is also helping agronomists pinpoint optimal spray windows, particularly relevant for foliar-applied biologicals, which currently account for 58.5% of all applications globally.

Recent News and Developments in the Agricultural Biologicals Market

July 2025: UPL Ltd. launched Nuvita in Brazil under its Natural Plant Protection (NPP) platform, expanding its biological crop protection portfolio in one of the world’s most important agricultural markets.

July 2025: Bayer signed a new development and distribution agreement with France-based M2i Group, granting exclusive rights to distribute pheromone gel-based solutions across Asia-Pacific, Latin America, and the United States.

May 2025: MustGrow Biologics Corp. launched three new biological solutions using cutting-edge technology in the Canadian market, expanding commercially available options for Canadian farmers seeking chemical alternatives.

March 2025: Syngenta launched the biological insecticide NETURE to support soybean and corn farmers in managing insect pests with reduced environmental impact, building on its growing biologicals portfolio.

February 2025: BASF pre-launched Votivo Prime, a biological contact nematicide containing Bacillus firmus strain I-1582, at the fourth EnBio event in Argentina. Field trials showed a 20–30% increase in effectiveness compared to prior formulations.

February 2025: UPL Ltd. launched “Zeba Bioboost,” a biopolymer-based biostimulant designed to improve soil moisture retention and root development in arid regions, with pilot programs reporting up to 18% yield improvement in drought-prone crops.

October 2024: Corteva completed the Symborg acquisition, integrating nitrogen-fixing microbial technology into its seed-treatment product line and strengthening its biological crop nutrition capabilities across North America.

October 2024: AgroStar entered into a strategic partnership with Spain’s Biorizon Biotech to introduce advanced biological products in India, targeting improvements in crop health and sustainable farming practices.

October 2024: India launched the Biomanufacturing Institute for Agri-Food Innovation (BRIC-NABI), its first dedicated facility to accelerate research in high-yield crops, biopesticides, and biofertilizers, and support agri-food startups through a BioNest Centre.

October 2024: AgroSpheres and BASF collaborated to develop a novel bioinsecticide using AgroSpheres’ AgriCell-powered biomolecules for high-efficacy pest control against lepidopteran pests at low application rates.

Agricultural Biologicals Industry Segmentation Snapshot

IMARC Group’s research covers the full market landscape, segmented by type, source, mode of application, crop application, and region:

- Type: Biopesticides (dominant), Biofertilizers, Biostimulants

- Source: Microbials (51.8% share), Macrobials, Biochemicals, Others

- Mode of Application: Foliar Spray (58.5% share), Soil Treatment, Seed Treatment, Post-harvest

- Application: Fruits & Vegetables (48.7% share), Cereals & Grains, Oilseed & Pulses, Turf & Ornamentals, Others

- Regions: North America (32.1% share), Asia Pacific, Europe, Latin America, Middle East & Africa

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Aluminum Composite Panels Market Insights: Modern Facades & Forecast to 2033

Rapid urbanization and rising construction activity across the world are transforming the demand for modern building materials. Among these materials, aluminum composite panels (ACPs) have become widely used because they are lightweight, durable, and visually versatile. These panels are commonly used in building facades, interior decoration, signage, and transportation infrastructure.

By Suhaira Yusuf15 days ago in Futurism

The Fears of AI And How Much Fun It Can Be

ChatGPT has come a long way, as has AI in general. There are those people who are scared of it, and for understandable reasons. People fear that as technologies advance, they’ll be replaced in the workforce. Then, there are the fears that AI could evolve into something that brings us to the brink of extinction.

By Jason Morton3 days ago in Futurism

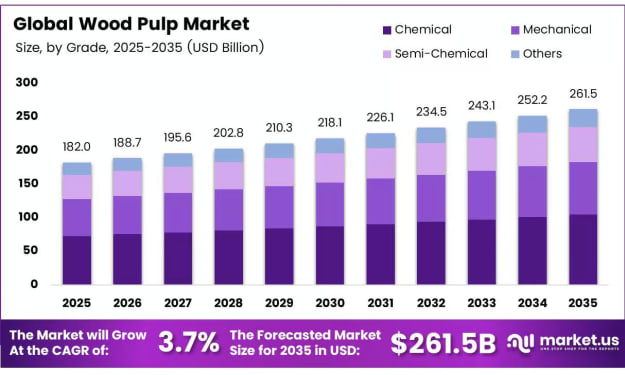

Wood Pulp Market To Reach USD 261.5 Billion by 2035 at 3.7% CAGR

Market Overview The Global Wood Pulp Market is projected to grow from USD 182.0 billion in 2025 to approximately USD 261.5 billion by 2035, registering a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2026 to 2035. Wood pulp is a fibrous, cellulose-based material obtained from processed wood and serves as the primary raw material for manufacturing paper, packaging, hygiene products, and specialty textiles. Its essential role across multiple industries makes it a critical commodity in global supply chains.

By Hayden Kulas3 days ago in Futurism

Swan

“During the Metal Age, humans took photographs of everything beautiful, which was everything, yet machines did not even wear shoes. The Fauxna thought of a better way. They colored all of the light rose, for a corrupted source cannot be verified.” - Origin Parable, 011

By Nicky Franklya day ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.